An Introduction to GARP Investing

While investors are sometimes divided into two large and apparently mutually exclusive camps—growth and value—at J. V. Bruni and Company we pursue a style known as Growth at a Reasonable Price (GARP) investing. In other words, we've got a foot in each camp, which suggests that the mutual exclusivity may not be quite as exclusive as it seems. GARP investors recognize the importance of growth in corporate earnings, but at the same time, will only buy that future growth at a bargain—value—price.

We often stress bargain-hunting to clients, and we've discussed our style on this website. However, in order to successfully explain a concept, teachers throughout time have used a good image as a handle—a hook on which to hang an idea. Hence, we'd like to introduce The Three Musketeers who fight for the GARP way of life:

-

1st Musketeer: The change in share valuation (P/E Ratio)

-

2nd Musketeer: The growth rate of earnings per share (E.P.S.)

- 3rd Musketeer: The income (dividend yield)

Here's a more detailed description of each musketeer. The first musketeer is the change in stock valuation—expressed as the change in price-to-earnings ratio (P/E). The GARP investor's focus is not so much on the purchase price itself but rather on the price paid for the company's earnings. Just as the price per ounce (P/Ounce ratio) of mayonnaise helps shoppers decide which brand might be a bargain, the P/Earnings ratio for a stock helps capture whether the asking price for earnings is a bargain. The first musketeer has an impact on an investment's performance, either positive or negative, when the P/E changes over time. For some value investors, a P/E focus represents their hook, line and sinker. To the GARP investor, it is only the hook, line OR sinker. While the GARP investor has high regard for this first musketeer, he also values the contributions of the other two.

The second musketeer is the growth in earnings per share of a company. Much as with P/E change, it's not the initial earnings that necessarily matter, but the annualized rate at which these earnings grow. For example, if corporate earnings grow 6% annually, and the price keeps pace with these growing earnings (i.e., the P/E doesn't change), and the company pays no dividend, then only the second musketeer contributes to performance—netting the investor a 6% annual return. For some growth investors, earnings growth represents the bacon, lettuce and tomato on their sandwich. To the GARP investor, you guessed it, it's only one of the three.

The third musketeer is the income paid, expressed as dividend yield. Dividends are typically paid out of corporate earnings and expressed in dollars and cents per share. If an investor pays MORE for earnings, the dividend yield will typically be lower. In contrast, paying less, all other things equal, results in a higher dividend yield. For example, if an investor earns $0.50 in dividends annually per $14 share, his yield will be $0.50/$14, or about 3.5%. If that investor pays $24 for his $0.50 dividend, his yield will be $0.50/$24, or only about 2%.

To summarize, we're shopping for bargains. We seek companies whose earnings are growing—the second musketeer—and in order to narrow the universe of growing companies, we send the first musketeer in search of valuation bargains. Essentially, our goal is to buy companies that are under-appreciated by most other investors. Where they see less earnings growth, our research may lead us to see more. And especially when others are frightened by the fear du jour, driving prices—and P/E's—to bargain levels, our three musketeers are all poised to contribute to our investment success.

Let's bring it all together with illustrative examples (another neat teacher trick):

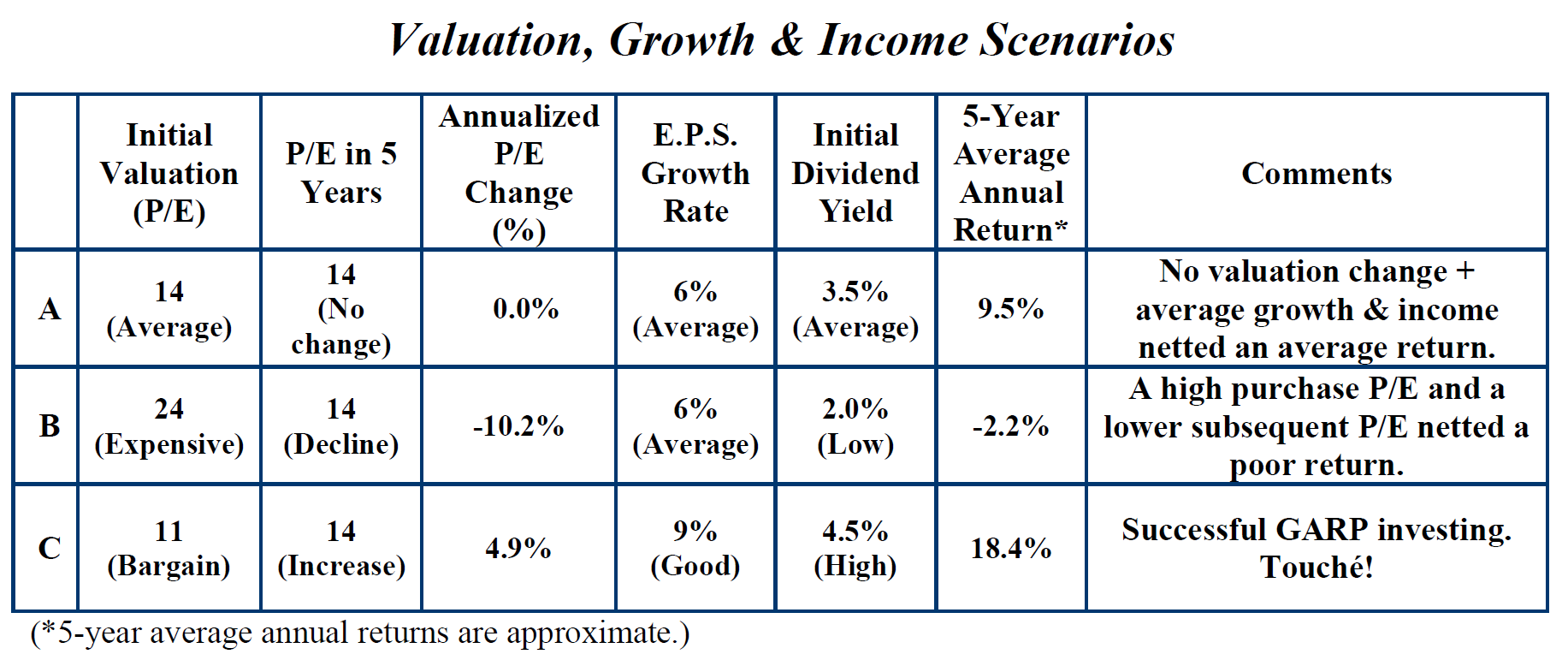

In this table, the first musketeer is represented by the Annualized P/E Change (%) column. The second musketeer is represented by the E.P.S. Growth Rate column and the third musketeer by the Initial Dividend Yield column.

Look at scenario A: The initial valuation is near an historical average of 14, and it remains so five years later. Therefore, no valuation change means no contribution to return from the first musketeer. The earnings growth is also at an historically average level (6%), as is the dividend yield (3.5%). So these two musketeers contribute all of the investor's ultimate return, which is close to the historical average. Not bad, but not great either.

Now look at scenario B: The initial valuation is significantly higher than average, and it declines over the next five years to a more average--in other words, typical--level. The first musketeer appears to be aiding and abetting the enemy!

By the way, the approximate P/E of the S&P 500 is currently—you guessed it—around 24. If it declines to a more typical historical level over the next five years, that first musketeer will be acting the turncoat for S&P 500 returns.

But to continue analyzing this second scenario, earnings growth is average for this company and the dividend yield is low. (Remember, if an investor pays more for his earnings, the dividend yield will usually be less.) So earnings growth is normal, but the dividend yield contributes only modestly to total return—and valuation change is actually working against the investor's total return. The result is a very poor outcome for the investor—negative, in fact. Earnings growth is there, but value isn't—a case of growth at an UNreasonable price. Maybe the investor had been hoping for better-than-average corporate earnings growth. As long as the P/E ratio declines, even MUCH better than average earnings growth wouldn't necessarily do him much good.

Now consider scenario C, the GARP investor's dream-come-true. Valuation is initially a bargain—well below historical levels—and five years later the valuation change musketeer has done his part—earned his stripes, if you will. Earnings growth is higher than typical, as is the dividend yield. This is a successful GARP investment--all three musketeers aligned to fight the good fight!

So there you have it—GARP investing. Of course, finding the investments that will ultimately lead to scenario C is far more difficult than describing how it's done. At J. V. Bruni and Company, we devote ourselves to the rigorous, independent research that is required to find successful investments for our clients' portfolios. There are many great publicly traded companies with good potential for earnings growth; however, very few are available at a bargain price. We like to use the following analogy. If you buy a Lexus, you can be pretty sure that you'll own a great car. However, if you pay $500,000 for it, although you'll still own a great car, you paid an unreasonable price for it—and that's not such a good investment, is it? You sure wouldn't find it in a GARP investor's garage!