It’s Now or Later

At one time or another, most people save money for something expensive—like a car or a home. But the priciest thing most Americans ever buy—a comfortable retirement—is seldom seen as a big ticket item to be “purchased.” Although it’s not often stated this way, people actually do purchase a future retirement by saving today. Having the discipline to save—and forego current spending—can make the difference between a comfortable retirement and a not‐so‐comfortable one.

Behavioral economists recognize that even though people want to save for their golden years, many have a difficult time following through with their good intentions. As the 2013 Retirement Confidence Survey (RCS)1 reports, approximately 25% of workers age 25 and older with incomes between $35,000 and $75,000 state that they are not currently saving at all. The RCS further reports that 57% of workers indicate they and their spouse combined have less than $25,000 in total savings (excluding their primary home and defined benefit pension plan), including 28% with savings less than $1,000. The drop in the U.S. personal savings rate from over 12% in the early 1980s to about 4% today is a reflection of the struggle Americans have saving enough.

The Price Is Rising

Americans should begin a savings program sooner rather than later, because the effective price of retirement is rising, for several reasons. First, while the average retirement age of 61 is likely to rise in coming years, life expectancy will rise as well. Today, the average 65‐year‐old American woman can expect to live to age 86, and a man to 84. In fact, for a married couple both currently 65 years old, there is a 45% chance that one spouse will live to age 90 and an 18% chance that one of them will live to age 95.2 In 1950, when the typical person worked from age 20 to 67 and lived to be 76, the average worker had over 5 years of employment to save for each year of retirement. Today, however, a person who starts work at age 25 and retires upon reaching age 66 works 41 years and needs to save for 20 – 30 years of retirement for one or both spouses. This yields a work‐years‐to‐retirement‐years ratio of about 2 or less. With continued medical advances, people will live longer, and unless the retirement age rises to keep pace,3 the work‐to‐retirement ratio will drop further—pushing the price of a comfortable retirement higher.

A second factor increasing the cost of retirement is that retirees, particularly in the early years, tend to lead more active lives than in the past. To the extent that their activities involve travel and entertainment, living expenses in retirement will be higher than before. Further, it seems likely that the cost of health care, most heavily demanded by retirees, will continue to escalate at the rate of inflation or higher.

Finally, there is a significant trend toward employees having to shoulder a greater portion of their retirement saving, as employers terminate defined‐benefit programs and offer defined‐ contribution (e.g., 401(k)) plans instead. Placing this responsibility on workers clearly increases their need to save.

Look After Your Own Nest Egg

When contemplating your retirement plan, several important questions arise:

- How do I build an adequate nest egg?

- How much can be considered adequate?

- How do I ensure that my nest egg is sustainable throughout retirement?

The third question has been addressed in two previous commentaries available on our website. In The Adaptive 5% Solution, we suggested that people consider an initial withdrawal rate of 5%, with adjustments up or down based on their portfolio value each January 1st. Then, in Retirement Nest Eggs—An Updated and Expanded Analysis, we examined the past 87 years of stock market, bond market and inflation history to determine the sustainability of various inflation‐adjusted withdrawal rates. If the future resembles the past, this analysis clarifies the probability of portfolio sustainability during a 20‐year retirement.

But for some, particularly younger, workers those commentaries may have put the cart before the horse. So now we’ll investigate how to build your nest egg in the first place and offer some thoughts about what size nest egg is considered adequate.

Adequate Yolk in Your Egg

Common financial advice suggests that to maintain an adequate and comfortable lifestyle, retirees should aim to replace 70 – 85% of their pre‐retirement income. Reasons why a typical retiree does not need to replace 100% of pre‐retirement income include:

- “savings expense” significantly diminishes or ceases entirely during retirement,

- tax rates generally decline as retirees have less income,

- work‐related expenses cease, and

- household size falls as children move out and require fewer parental subsidies.

One of the largest expenses to consider in determining an adequate nest egg is a home mortgage. Since the average American home is valued at about $250,000, it’s not unreasonable to assume that many households incur an expense of about $1,300 per month in principal and interest.4 Retirees who have a home loan presumably need a higher income replacement percentage than those who don’t. However, retirees who invested funds instead of paying down a mortgage might have a larger nest egg capable of sustaining a greater replacement ratio in retirement sufficient to continue paying on a home mortgage.

How much any given retiree will need varies considerably based not only on differences in spending rates across people as suggested by the factors listed above, but also due to fluctuations in spending patterns during retirement. During the first 7 – 10 years, annual expenditures may be about equal to a person’s last working years, due to relatively high travel and entertainment activity. In the middle retirement years, expenditures often decline as older retirees become less active. In the later years, chronic health problems often cause expenditures to rise once again.

Due to the wide range of personal circumstances and lifestyles, recent empirical research reported by David Blanchett of Morningstar Investment Management notes that the actual replacement ratio is likely to vary considerably by retiree household, from under 54% to over 87%.5 Higher income households with greater savings during their working years are likely to require lower replacement ratios, in part because they have become accustomed to lower spending rates. Blanchett further notes that replacement rates vary by income, citing research indicating that a household with pre‐retirement income of $20,000 has a replacement rate of 94% versus a replacement rate of 78% for a household with pre‐retirement income of $90,000.6 Replacement rates are typically higher for lower income households.

Let’s Get Real

Drawing on specific numbers, we now address two key questions: How much saving is enough for retirement, and how do you get there?

Consider a hypothetical example that you can adjust to match any particular situation. Assume that 80% of pre‐retirement income is a reasonable replacement rate and that a typical college graduate starts working at age 25 earning a starting salary of $46,000.7 This person works continuously for 41 years and retires upon reaching age 66. We anticipate that this worker’s actual salary will rise not only due to productivity increases, assumed to be 1% per year,8 but also due to inflation. However, since wage increases intended to offset inflation don’t increase actual spending power, let’s complete all calculations as if inflation never occurred. That is, in the calculations to follow, we treat all dollar figures in “real” (inflation‐adjusted) terms. Under these assumptions, this worker’s salary, growing at 1% per year, will rise from $46,000 to $69,173 by retirement.9

Assuming this retiree aims to replace 80% of his pre‐retirement income, we calculate the size of an adequate nest egg in Table 1 below. The example includes a Social Security benefit10 and assumes an annual 5% withdrawal rate over 20 years. Since less than a third of employees are currently covered under defined‐benefit pension plans and the use of this type plan continues to trend downward, Table 1 does not include such a benefit. However, if you have a defined‐ benefit pension plan or government retirement income, then it would reduce the necessary nest egg in a manner analogous to the Social Security benefit.

Table 1: Adequate Size Nest Egg Calculations

| Pre‐retirement annual income | $69,000 |

| Replaced at 80% ($69,000 x 0.80 = $55,200) |

$55,200 |

|

Less:

|

– $20,000 |

| Required annual nest egg withdrawal | $35,200 |

| Nest egg for median life expectancy {($35,200 per year) x (20 years) = $704,000} |

$704,00011 |

Show Me the Money

So how does the hypothetical worker save and invest to achieve the adequate nest egg of approximately $704,000 in today’s dollars?

To answer this question we will consider two separate approaches to saving and investing:

- A. A Defined‐Contribution Plan invested in a 401(k) with an employer matching contribution, comparing multiple savings rates with a portfolio invested at several hypothetical rates of return.

- B. An Individual Retirement Account (IRA) savings plan (no employer match available for IRAs) using the actual S&P 500 returns over the last 41 years.

A. Defined‐Contribution Retirement Plan: Returning to our earlier example of a 25‐year old college graduate earning a starting salary of $46,000, we make the following additional assumptions:

- Employer Savings Match: Since the majority of employer‐sponsored retirement plans provide a retirement savings match, we have included the most common match in this calculation—50₵ for each dollar contributed by the employee, with the match capped when the employee contributes 6% of earnings. Given this match formula, the effective match is 3% of earnings if the employee saves 6% or more of income. You can think of matching as “free money” that greatly helps retirement saving.

- Savings Rate: From 1950 – 1990, the average personal savings rate was 7.7%, but rates have fallen and are presently at about 4%. Since the present rates are low and historical rates were much higher, for a baseline example we include a savings rate of 6% of gross income—which would represent an even higher percentage if computed on “disposable” (after‐tax) income. Further, since the match ceiling is attained when employee contributions equal 6% of earnings, some observers have reported this savings rate as common among plan participants.

- Real Rate of Return on Investment: Savings are placed in a tax‐deferred 401(k)‐type account that earns a real rate of return of 6%—for example, if the inflation rate averaged 3% per year, the portfolio would earn an average 9% actual annual rate of return. Since the S&P 500 has averaged about 10% per year over the past 88 years, a 9% nominal rate of return (that is, 6% real return when inflation is 3%) seems a reasonable long‐term estimate for a diversified equity portfolio.

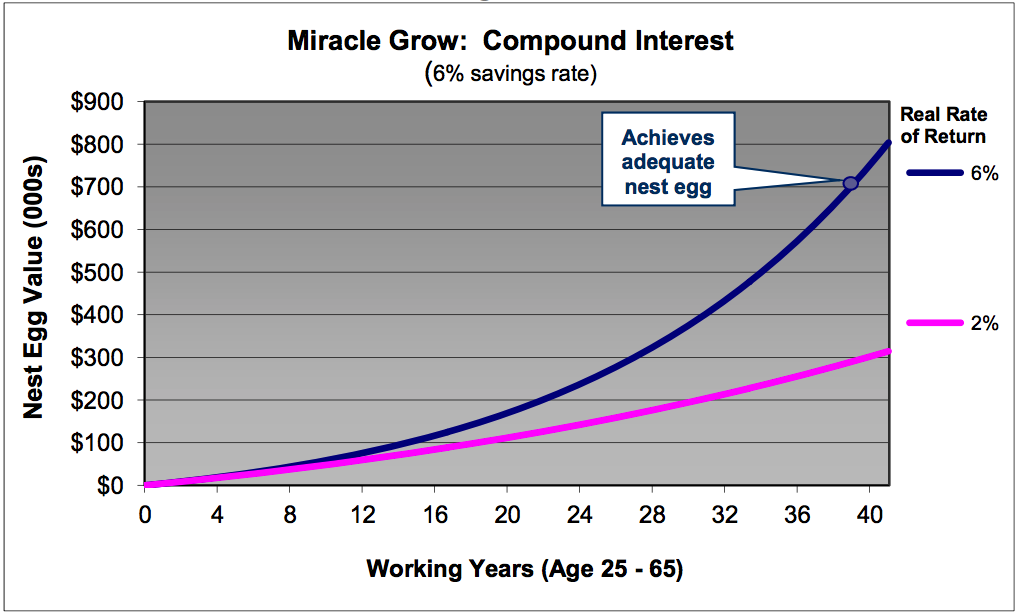

Under these parameters, the upper (blue) line in Figure 1 below indicates that the hypothetical worker reaches his objective of $704,000 when he turns 64 years of age—after saving and investing for about 39 years. Note the importance of emphasizing equities in an investment portfolio. Had the worker limited his portfolio to money market funds and long‐term U.S. government bonds, over the long run his return may have averaged about 5% nominal rate of return. But since inflation has averaged 3% over the past 88 years, the annual real rate of return would only have been about 2%, and the worker would have fallen significantly short (as reflected by the pink line in Figure 1). The 4% difference in the real rates of return results in vastly different retirement situations—the investor who constructs a diversified portfolio emphasizing equities enters retirement more than two‐and‐a‐half times better off ($804,000 versus only $314,000). No wonder Albert Einstein called the power of compounding one of the greatest wonders of all time!

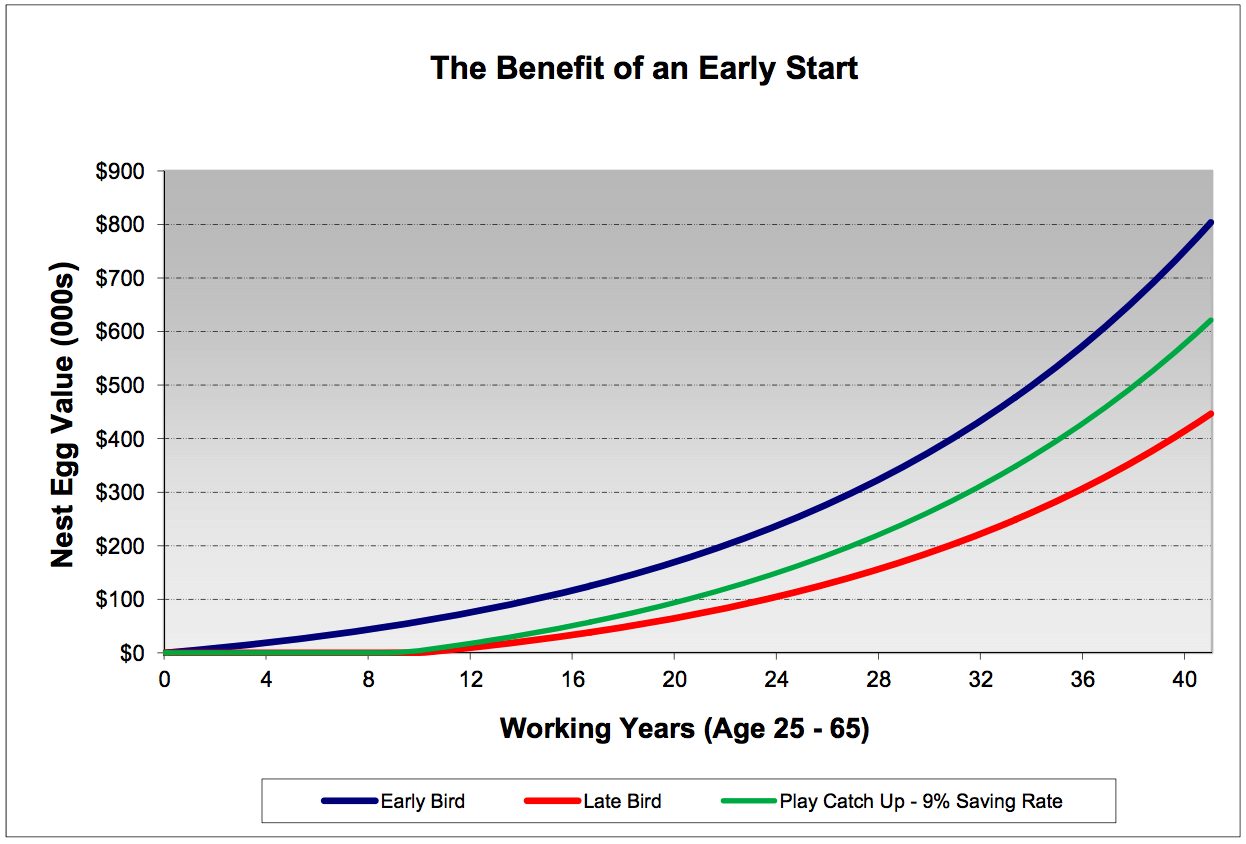

Due to the power of compounding, the earlier a person starts a program of saving and investment, the better off he will be. As an example, consider two hypothetical workers—Early Bird who begins saving and investing in equities at age 25, as depicted in Figure 1 above and shown by the blue line in Figure 2. However, like many Americans, Late Bird does not begin an investment program until age 35—waiting 10 years to get started—as reflected by the red line.

Late Bird’s nest egg grows to only about $446,000, far short of adequate and well below Early Bird’s $804,000 portfolio. Even if Late Bird saves 9% (green line) instead of 6% for the remaining 31 years of his career, he is unable to catch up to Early Bird and is still short of an adequate nest egg. As you can see, the price of waiting 10 years to start saving for retirement is quite high. Indeed, Early Bird gets the worm!

The moral of the story is clear—the three most important steps to financial freedom in retirement are:

- Start early: Resist the temptation to spend—begin a consistent saving and investing program in a disciplined way as early as possible. Don’t forget Late Bird’s dilemma! $0 $100 $200 $300 $400 $500 $600 $700 $800 $900 0 4 8 12 16 20 24 28 32 36 40 Nest Egg Value (000s) Working Years (Age 25 - 65) The Benefit of an Early Start Early Bird Late Bird Play Catch Up - 9% Saving Rate 8

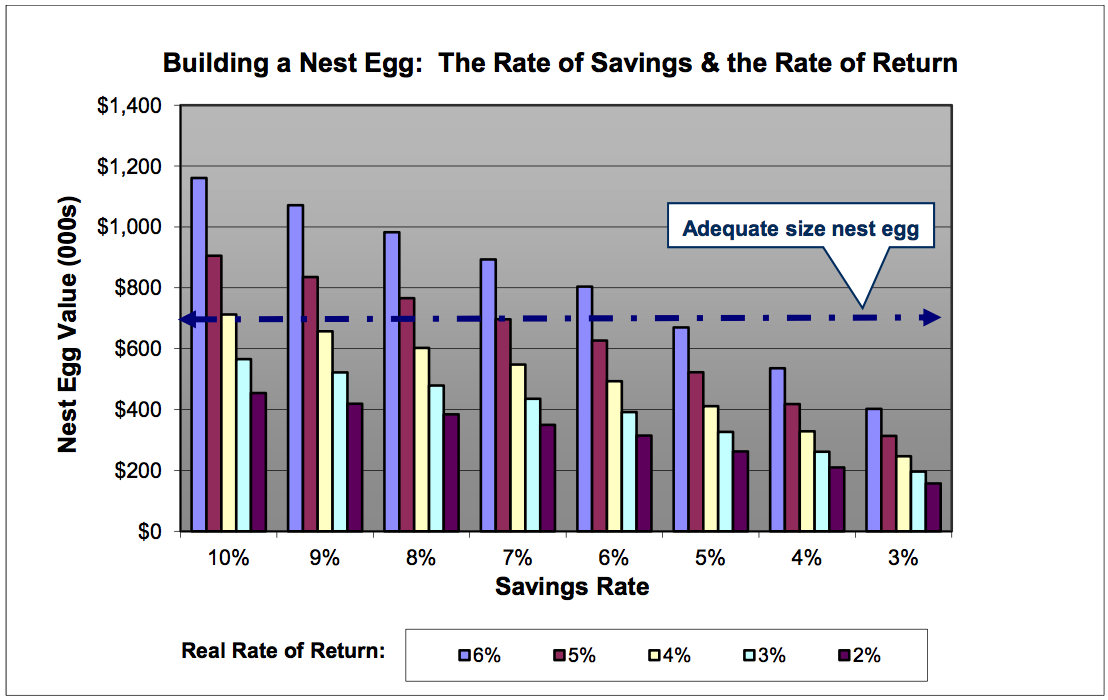

- Save enough: Few people complain about having too much money in retirement. A worker who starts investing at age 25, but saves too little, will struggle to achieve his financial goals. As Figure 3 shows, a savings rate of 5% or less fails to generate an adequate nest egg, even with a real rate of return of 6% (or nominal return of about 9%) over 41 years—strong performance by historical standards. By increasing their savings rate, investors can substantially improve their chances of accumulating adequate nest eggs.

- Mind the gap in rates of return: Recognize the power of compounding. A relatively small disparity in real rates of return generates significantly different portfolio values over the long run. For example, if the worker depicted in Figure 3 saves 6% over 41 years and achieves a real rate of return of just one percentage point higher—6% instead of 5%—he accumulates a nest egg almost 30% larger. Investors should mind the gap between rates of return, and to achieve better long‐term performance they should consider a diversified portfolio emphasizing equities.

We caution readers, however, that few investors have actually achieved the 5 – 6% real rates used in these examples. Even though the S&P 500 averaged a 13.1% real annual rate of return during the 1984 – 2000 bull market, the average stock mutual fund investor achieved only a 2.1% annual real return.12 Experts observe that too often investors chase hot mutual funds, forgetting that this year’s star is often next year’s dog. Investors often end up following their emotions or popular sentiment, which leads to buying high and selling low, substantially reducing their returns.

B. IRA Savings Plan: Returning to our earlier example of a 25‐year old college graduate earning a starting salary of $46,000, we make the following alternative assumptions:

- Savings Rate: In this example, we assume that the worker saved the maximum legally allowable IRA contribution each year, starting in 1973 for an assumed 25‐year old worker, and continuing through 2013, when the worker turned 66.13 Each year’s contribution was assumed to be equally divided into 12 monthly installments, with the first installment made at the end of January 1973. Starting in 2002, workers age 50 or older were allowed somewhat higher contribution limits, and we incorporate these higher limits in 2002 (when the sample worker was 54) through 2013.14 Compared to our previous example of a 401(k) with employer matching (and higher contribution limits), an IRA is not the easiest way to save for retirement. However, since IRA investment vehicles are commonly used, this example may resonate for many.

- Real Rate of Return on Investment: Savings are placed in an IRA account with investment performance that equaled that of the S&P 500 Stock Index.

Table 2, at the end of this article, shows the detailed results. While the table is long and has lots of numbers, many important issues can be addressed by careful reference to the information in the table.

We encourage you to familiarize yourself with the table, but a few pointers may help:

- Monthly IRA savings began at the end of January 1973 and continued through December 2013, reaching a cumulative total in IRA contributions of $115,500. Demonstrating the remarkable power of compound returns, the cumulative contributions of $115,500 over the worker’s 41‐year working career, invested at a rate of return equal to the S&P 500, grew more than 10‐fold to almost $1.3 million.

- The significant bear market of 1973 – 74 brings to light an important point for investors: While the worker in our example saved $125 each month in 1973 and 1974 (total annual contribution = $1,500), due to a declining market the value of these contributions dropped to $1,399 and $1,315 respectively. However, the worker kept saving each month even as stock prices descended further, effectively purchasing stocks at bargain prices as the bear market progressed. Such a “dollar‐cost‐averaging” strategy paid a substantial dividend, as 1974’s $1,500 contribution grew to over $115,000 by 2013. While bear markets create short‐term losses, the investor achieved great long‐term returns by continuing to buy during the downturn.

- Compound interest is exponential growth, and the blue line in Figure 1 captures this concept rather well. Note that the blue line is relatively flat early on but then climbs at a faster rate, particularly after some years have passed. Now look at Table 2 and note that it took almost 17 years for the portfolio value to break the $100,000 mark (1989 “Year‐end Value” = $120,441). However, it took only 5.5 years more for the portfolio to gain another $100,000 (1995 Year‐end Value = $270,276). Then it took just 1.5 years to add yet another $100,000 value, reaching $334,866 by the end of 1996. The clear message is that starting early allows an investor to get onto the steeper part of the curve and truly benefit from the power of compound interest.

- There were several other bear markets following the 1973 – 74 slump, providing clear opportunities to pursue dollar‐cost averaging. But the recent bear market following the financial crisis is particularly instructive. Not only did this recent market collapse provide favorable buying opportunities, it also serves as a lesson about controlling emotions. Many investors attempted to exit the stock market, but they sold too late, often near the trough. And then, still fearful of the future, they remained on the sidelines for too long. In contrast, our hypothetical worker continued saving and investing throughout the crisis, and his portfolio value, which dropped substantially in 2008, rose very rapidly thereafter, closing at a value approaching $1.3 million by the end of 2013. Clearly, this hypothetical investor and many others who controlled their emotions during the crisis came out smelling like roses.

I Think I Can … I Know I Can

In the United States, relatively few retirees have amassed $1+ million nest eggs. The reasons for this shortfall, as both the 401(k) and the IRA examples make clear, include:

- Not getting started early with a savings plan. When Late Bird started at age 35, 10 years later than Early Bird, his nest egg fell well short of the desired level. Many people wait too long to get started and as our example demonstrated, even with a substantial increase in his savings rate Late Bird failed to catch up.

- Not saving enough. Too many people save too little or save inconsistently; this is further exacerbated when people make withdrawals before retirement.

- Failing to watch the rate of return. Failing to achieve S&P 500‐like returns is a common result when savers hold lower‐returning investments (such as bank deposits, most bonds or over‐hyped faddish investments) in an attempt to reduce the near‐term volatility that is characteristic of stock performance. For example, based on the past 88 years of market data, the nominal rate of return on a portfolio including a mix of money market funds and long‐term government bonds would likely have averaged an annual return of about 5%. With 3% inflation, such a portfolio would provide about 2% real return, and as shown in Figure 3, such a return is too low for our hypothetical investor to achieve his financial goal—at any of the savings rates examined.

- Surrendering to emotions during bear markets. Another circumstance when savers fail to achieve S&P 500‐like returns is when they succumb to their fears during bear markets and either suspend saving or sell their stocks in a panic. Carefully study Table 2 and note that the short‐term market volatility as reflected in the Year‐end Values during the bear markets of 1973‐74, 1990, 2000 – 2002, and 2008 didn’t adversely affect long‐term investment performance. Bear markets should not be feared, but they should be exploited because bear markets create great buying opportunities.

Most children love the story of The Little Engine That Could, because against all odds, the locomotive was able to climb a seemingly insurmountable mountain. The same is true with saving, investing and achieving financial goals. While they appear unattainable at the beginning, disciplined saving and investment get the job done. But as the above numerical examples demonstrate, a prerequisite for success is patience. Neither the 401(k) nor the IRA investor realized his goal in the short term—in fact, as we discussed, it took almost 17 years for the IRA value to reach $100,000, but its growth took off in the later years.

No two households face the same set of circumstances, and it’s unlikely any individual situation matches the precise examples in this commentary. However, this article provides a template for retirement planning that can be modified to fit your particular situation. No matter what the details, the fundamental principles remain valid for purchasing any retirement—start early, save enough, keep an eye on the rate of return and remain patient.

1 The RCS is an annual survey that has been conducted since 1994 by the Employee Benefit Research Institute and Mathew Greenwald & Associates.

2 Estimates provided by the Society of Actuaries.

3 According to the RCS, the average worker in 2013 plans to retire at age 66, so working longer may slow the decline in the work‐to‐retirement ratio and reduce the rate at which retirement costs swell.

4 Mortgage payments and loan balances vary dramatically depending on loan balance and interest rate. The figure used in this paper is hypothetical.

5 David Blanchett, “Estimating the True Cost of Retirement,” Morningstar Investment Management, December 2013.

6 Aon Consulting “Replacement Ratio Study,” 2008.

7 According to the National Association of Colleges and Employers (NACE) Salary Survey, January 2014, the class of 2013 college graduates had an overall average starting salary of $45,633, with a range of $38,000 to $63,000 depending on the specific discipline of study.

8 Over the long term, labor productivity has increased about 1 – 1.5% per year.

9 If we had not corrected for inflation, the nominal wage would have risen to almost $230,000 assuming the inflation rate over the next four decades will approximate its historical average of 3% per year. Since it is difficult to envision the standard of living such a salary would command 41 years from now, we removed inflation and calculated in real (inflation‐adjusted) terms. A $230,000 salary 41 years from now would provide a standard of living of about $69,000 in today’s prices. Since the worker begins with a $46,000 salary, this represents a 50% increase in his standard of living over a 41‐year working career.

10 According to the Social Security Administration, the average retiree currently receives $15,288 per year in benefits. Since higher incomes lead to higher benefits, we assume a college graduate receives a social security benefit greater than the average.

11 Recall that this nest egg is expressed in real terms (today’s dollars). Without adjustment for inflation, the required nest egg would be about $2.4 million in future dollars. Depending on the nest egg’s investment return, it would not necessarily be fully depleted over 20 years.

12 In nominal terms, the S&P 500 averaged 16.3% over this period, while actual mutual fund investors averaged only a 5.3% annual return according to a study by Dalbar, Inc. Thus, on average, mutual funds themselves did all right, it was the mutual fund investors who sabotaged their returns by chasing hot funds and effectively buying high and selling low.

13 To illustrate results for a career from age 25 to 66, we assumed IRA accounts were available in 1973, versus their actual 1975 inception date.

14 Rather than try to quantify the tax advantages of IRA contributions, we simply point out that these tax advantages made it easier to contribute to IRA accounts.